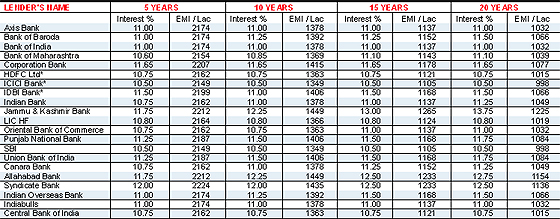

Table of Content

In the case of a fixed-rate loan, the lock-in period is the same as the loan period because the loan duration is by default the lock-in period for fixed-rate loans. Hence, if you took a 5-year fixed-rate loan, then the lock-in period is 5 years. Sometimes, home loans comes with no lock-in periods, but borrowers would still have a legal clawback feature to contend with.

One of HDB's objectives is to to provide affordable housing for the people. This lock-in period is usually active during the initial few years of the loan’s lifetime. Lock periods involve several important variables and a borrower should be aware of the trade-offs that occur when changes are made.

Lock Period

This indirectly acts as a lock-in period as the borrower would still have to incur penalties should the loan be redeemed within the legal clawback period. This really depends on how the lender decides to design their loan packages. While this looks like a hefty penalty, it can be worthwhile if the borrower has found a much better loan or that he has decided against buying the property altogether.

In general, it is a valuable tool for the borrower and one worth pursuing. Don’t look at lock-in periods as a major deliberation factor, so much so that it impedes you from achieving what you want. There’s a good chance that the lock-in period will not affect you at all. Two years down the road, you come across a much better deal, and you’re itching to refinance. SOR rates are calculated with a complex financial formula, solved with simple algebra. The results of solving the equation therefore depends on the inputs used.

How Lock Periods Work

A lock-in period is a period of time within the tenure of a home loan in which repayment of the loan would result in penalty charges incurred by the borrower. A mortgage rate lock float down product gives borrowers security and flexibility when rates increase and fall during the lockdown period. A lock period refers to an amount of time during which a mortgage lender must guarantee a specific interest rate or other loan terms open to a borrower. For under construction property loans, which refer to loans for property that are still under construction, mortgages usually don’t come with any lock-ins.

This means you wouldn’t need to pay the penalty of 1.5% on the loan amount redeemed. Refinancing occurs when you switch to another bank while redemption happens when you’ve decided to sell off the property. A shorter lock period, from one week to 45 days, will generally feature a lower guaranteed interest rate and possibly lower fees. Many lenders will charge no fees at all for a lock period of fewer than 60 days. If the lender is not able to approve the application during the lock period, though, the borrower will once again be exposed to interest rate risk. To extend the lock period, a borrower may choose to pay a fee, or lock deposit.

If there’s a penalty, why do people still sign up for loans with lock-in periods?

As explained above, the lock-in period is 5 years since this is a fixed-rate loan. It would be more worthwhile to wait out the lock-in period before refinancing. For example, a fixed rate housing loan with the first 3 years at 2% and thereafter SIBOR + 1% would have the lockin period during the first 3 years of fixed rates. With fixed rate home loans, the lock in period is almost always during the years where the fixed rates are applied.

A longer lock period, between 45 and 90 days, offers greater protection. Generally, though, a lender will not offer as attractive an interest rate over an extended lock period. If the parties are unable to close on the loan during this period, the lender may be unwilling to extend a second lock offer at a rate attractive to the borrower.

As far as you’re concerned, you’re satisfied with the rates for the first 3 years. You know that rates only shoot up from the fourth year onwards, but by then, your lock-in period is over and you’re free to shop around for a better deal. Take note too that some banks may impose additional fees on top of this penalty.

The penalty fees can come as either a cancellation fee, break costs or a redemption fee. A locked-in interest rate occurs when a lender agrees to provide a certain loan rate as long as the homebuyer closes by a set deadline. Despite the inflationary times, looming recession, ongoing interest rate hikes and seventh lunar month, condo property sales... They want to enjoy the promotional rate, which is usually 0.3% lower than those without lock-in periods. Our opinion is to always take a HDB concessionary loan if you are eligible for one.

A lock period offers the borrower peace of mind when it comes to protection from rising interest rates while the lender processes the loan application. Processing times vary by jurisdiction, but the length of the lock should roughly mirror local average approval periods. If rates fall during the lock period, the loan lock may offer options beneficial to the borrower.

Varying inputs that result from economic impacts and indicators can lead to negative value when the formula is solved. Key input indicators include USD/SGD spot rates and USD/SGD forward rates. Doretha Clemons, Ph.D., MBA, PMP, has been a corporate IT executive and professor for 34 years. She is an adjunct professor at Connecticut State Colleges & Universities, Maryville University, and Indiana Wesleyan University. She is a Real Estate Investor and principal at Bruised Reed Housing Real Estate Trust, and a State of Connecticut Home Improvement License holder.

What happens if you’re in urgent need of funds and have to sell off your house within the lock-in period? You’ll still have to pay the penalty unless there was a clause stating that you could get a waiver for such circumstances. In other words, read your contract carefully before signing on the dotted line if you feel that your situation may change in the near future. Depending whether you chose a fixed- or floating-rate loan, the lock-in period can be anything between 1 and 5 years.

No comments:

Post a Comment